Protecting Core Banking: From Implementation to Operations

Core banking platforms are among the most critical systems within any financial institution, yet security is often treated as a post-implementation concern rather than a foundational design principle. In this thought leadership article, cybersecurity expert Godfrey Kutumela explores the three disciplines that determine whether a core banking platform remains secure throughout its lifecycle: security governance from day one, zero-trust access and privileged access management, and end-to-end protection of data, integrations, and operational resilience. Drawing on global regulatory frameworks, industry best practices, and real-world banking security challenges, this article provides practical guidance for banks, fintechs, microfinance institutions, and digital banking programmes. It also includes a dedicated analysis of Apache Fineract and Mifos deployments, highlighting the unique security considerations of open-source core banking platforms. Whether you are planning a new core banking implementation or strengthening an existing environment, this article offers a roadmap for building a resilient, secure, and regulator-ready banking platform.

Godfrey Kutumela

6/4/202627 min read

Three Disciplines That Decide Whether the Ledger Survives Day One and Every Day After

There is a recurring pattern in banking technology programmes. The platform is delivered, the cutover is celebrated, and only then does security become a sustained conversation. By that point, the architecture has been frozen, the access model has been provisioned, the integrations have been built, and the operating runbooks have already been written. Security from that moment forward is largely a remediation exercise, conducted at a higher cost than design would have demanded, against a target that is now both more exposed and harder to change.

The security challenge is structural, emanating from how core banking implementations are governed as delivery programmes whose success is measured by functional go-live, schedule, and budget, with security treated as a workstream that must not delay the programme. The result is a system that meets the regulator's minimum baseline at go-live and then accumulates exposure across the operational decades that follow.

Modern core platforms, whether legacy mainframe, modern Java stacks such as Apache Fineract, vendor suites such as Temenos, Finacle, Fiserv, FIS, Mambu, or Thought Machine, or hybrid combinations, share an uncomfortable security reality: the controls in place on day one will determine the institution's exposure for the next ten to twenty years. Configuration debt is the most expensive debt a bank carries, and it accumulates fastest in core banking.

This article makes a direct argument on this issue and proposes three security disciplines that will determine whether a core banking implementation will withstand the threats it will actually face:

1. Security governance built into the programme from day one

2. Zero-trust access with strong privileged-access controls

3. End-to-end protection of data and integrations, with operational resilience

None of the three is novel. All three are routinely under-built, and the cost of the under-build is paid in incidents, regulatory findings, and remediation programmes for years afterward.

| “The controls in place at core banking go-live decide the institution’s exposure for the next decade. Security must be a design discipline, not a cutover checklist.” |

Included in the article is a dedicated section that examines the Mifos/Apache Fineract environment specifically because open-source core banking carries security characteristics, both opportunities and exposures, that closed vendor stacks do not.

I. Why Core Banking Demands Its Own Security Discipline

Banks run on many systems, but the core banking platform is uniquely consequential. It is the system of record for customer accounts and balances. It posts and settles transactions. It enforces the bank's product rules. It feeds the general ledger, regulatory reporting, the data warehouse, and every customer-facing channel. Compromise it, and almost nothing the bank says about its financial position can be trusted.

This concentration of authority makes the core a high-value target. It is also a high-friction one. Core platforms are typically long-lived. They tend to integrate with hundreds of internal and external systems through interfaces of varying ages, protocols, and security maturity levels. They run on stacks ranging from modern cloud-native microservices to legacy systems that predate most of the people who maintain them. They are subject to overlapping regulatory regimes, each with its own audit cycle, terminology, and reporting requirements. And they cannot, under normal circumstances, be turned off.

The combination of high value, high integration, long life, and zero tolerance for downtime creates a security problem unlike almost any other in enterprise IT. The defender must protect a system that is too important to fail, too connected to isolate, and too entrenched to replace quickly against adversaries who understand all of this and design their campaigns accordingly.

Three categories of risk dominate:

Confidentiality risk arises because the core holds personally identifiable information, account details, and transactional history that have value on criminal markets and, increasingly, to state-sponsored actors building intelligence dossiers.

Integrity risk is the existential threat. An attacker who can silently modify ledger entries, alter interest calculations, or insert fraudulent transactions undermines the institution's reason for existing.

Availability risk is the operational threat. An offline core is a bank that cannot function, and modern customers do not tolerate even short outages.

Most public banking incidents are framed as confidentiality breaches because that is what regulators require to be disclosed. The integrity attacks, which are rarer, harder to detect, and often discovered only after significant damage, are the ones that keep experienced banking security leaders awake at night.

The Bangladesh Bank SWIFT incident of 2016, the various ATM cash-out campaigns attributed to Lazarus and FIN7 since 2018, and the procession of payment-system manipulations through correspondent banks all share a common pattern: the core itself was rarely attacked head-on. Systems and processes manipulated it using legitimate access.

II. The Three Disciplines That Decide the Outcome

Cybersecurity guidance for banking is voluminous. NIST CSF 2.0, the Basel Committee’s Principles for Operational Resilience, the FFIEC IT Examination Handbook, the EU’s Digital Operational Resilience Act, the SARB Prudential Authority’s Directive 1 of 2024, the Monetary Authority of Singapore’s Technology Risk Management Guidelines, ISO 27001, PCI DSS, the SWIFT Customer Security Programme, and dozens of national supervisory frameworks each contribute hundreds of pages of detail. An institution that attempted to operate against all of them simultaneously, without prioritisation, would struggle to finish reading the requirements, let alone implement them coherently.

Three disciplines, however, consistently distinguish core banking implementations that withstand operational reality from those that generate expensive remediation programmes after go-live. They are not exhaustive, and they do not replace the regulatory frameworks above. Those frameworks remain mandatory. But these three disciplines are the ones whose absence most reliably predicts the next incident: security governance from day one; zero-trust access with strong privileged-access controls; and end-to-end protection of data and integrations, with operational resilience.

Each discipline is examined in detail below, mapped to relevant regulatory expectations, and translated into implementation requirements that programme teams can use as gate criteria. The analysis then turns to Apache Fineract and Mifos specifically, because open-source core banking has become a material category in the global market, particularly across microfinance, digital banking, neobanking, and emerging-market deployments. Its security profile warrants explicit treatment, not as an exception to the three disciplines, but as a case where institutional ownership of those disciplines becomes even more visible.

The point is not that a bank can ignore the rest of the control universe. It cannot. The point is that successful implementation requires a hierarchy of attention. Some controls provide assurance only after the platform is already stable; others determine whether the platform can be trusted from the first day it processes real customer balances. In core banking, the latter must come first.

A programme that cannot demonstrate governance ownership, controlled access, protected data flows, secure integrations, and tested recovery before go-live has not implemented a secure core banking platform. It has implemented a functional one and deferred the security consequences into operations.

| “Security governance, zero-trust access, and end-to-end protection of data and integrations are not three of many disciplines. They are the three whose absence predicts the next incident.” |

III. Discipline One: Build Security Governance Into the Programme From Day One

Treat security as a core workstream, not a post-implementation audit item. This statement, simple in formulation, is the single most consequential decision in any core banking programme. It determines whether the security architecture has been deliberately designed against the threat model the bank actually faces or assembled around the architectural decisions the delivery teams happened to make.

Security ownership, regulatory obligations, risk appetite, control baselines, and acceptance criteria must be defined before design and build start. NIST CSF 2.0 organises this responsibility around six continuous outcomes — Govern, Identify, Protect, Detect, Respond, and Recover — and explicitly elevates Govern as the function that holds the rest together. Basel Committee and BIS guidance expect banks to maintain documented ICT and cybersecurity policies, clearly defined accountability, identification and protection of critical assets, tested incident response, business continuity, and disaster recovery. These are not optional inputs that arrive after the architecture is settled. They are the inputs that shape it.

| “Security governance is not the activity that comes after the build. It is the activity that decides what is built.” |

Mapping Controls to the Regulatory and Standards Baseline

A core banking implementation will be examined in operation against multiple frameworks simultaneously. The control mapping should be performed once, comprehensively, at the start of the programme, and maintained as a living artefact. The institution should be able to demonstrate, for each control in scope, which framework requirements it satisfies, who owns it, how it is tested, and where its evidence is recorded.

Typical control source frameworks for a core banking programme include:

NIST Cybersecurity Framework 2.0 — for the overall control taxonomy and the Govern, Identify, Protect, Detect, Respond, Recover lifecycle.

ISO/IEC 27001 and 27002 — for the information security management system and the operational control set, with ISO 27017 and 27018 extending into cloud environments.

PCI DSS v4.0.1 — wherever cardholder data flows through or is stored by the core, including the related encryption and key management requirements.

SWIFT Customer Security Programme — for institutions participating in the SWIFT network, with mandatory and advisory controls attested annually.

Privacy regulation — POPIA in South Africa, GDPR in the European Union, equivalents in each operating jurisdiction, with attention to lawful basis, data minimisation, retention, and cross-border transfer.

Central-bank expectations — SARB Prudential Authority Directive 1 of 2024 on cyber resilience and supplementary guidance notes for South African institutions; FFIEC IT Handbook in the United States; PRA SS1/21 and operational resilience rules in the United Kingdom; DORA Regulatory Technical Standards in the European Union; MAS TRM Guidelines in Singapore; CBN cyber risk framework in Nigeria; and equivalent supervisory expectations in each market.

Audit and assurance baselines — SOC 2 Type II, where the institution provides services to others, internal audit standards, and the external auditor's IT general control expectations.

The mapping exercise is not an academic one. It produces the control baseline against which design, build, testing, and go-live readiness will be measured. Programmes that skip this step typically discover, late in the cycle, that controls assumed to exist are not implemented, that overlapping frameworks have conflicting requirements that no one has resolved, and that the regulator's specific expectations were not incorporated. By that point, the cost of remediation is several times the cost of being properly mapped at the start.

Threat Modelling the Surface That Will Actually Be Attacked

Threat modelling is the most reliable predictor of which controls actually matter, and it is the single discipline most often skipped in core banking programmes because it is perceived as slow and unstructured. Done properly, it is neither. Using a structured method — STRIDE for component-level analysis, PASTA for risk-driven analysis, or attack-path analysis for adversary-driven modelling — the programme should produce, before detailed design begins, a documented view of how the system could be attacked, by whom, with what likelihood, and with what consequence.

For a core banking platform, the threat model must explicitly cover the surfaces that modern incidents exploit. These include the customer-facing and partner-facing channels (mobile, internet banking, USSD, agent banking, branch); the API layer and its integrations with channels, payment switches, card networks, fraud and AML engines, regulatory reporting, and analytics; the batch and end-of-day processing windows where reconciliation gaps are exploited; the database replication paths that often carry less monitoring than primary databases; the administrative consoles and operator interfaces where most insider abuse occurs; and the payment flows themselves, including SWIFT, RTGS, ACH, instant payment rails, and card scheme connectivity.

| “A threat model that does not cover the API layer, the batch windows, the admin consoles, and the payment flows is not a threat model. It is a vulnerability spreadsheet.” |

The output of threat modelling should feed three subsequent activities: the control set (which controls must be present, and where), the test plan (which scenarios must be exercised), and the monitoring baseline (which events must be detectable). When the threat model is treated as a one-time artefact filed at the start of the programme and never revisited, it adds little value. When it is maintained continuously through implementation and operations, it becomes the most useful security artefact the institution owns.

Secure SDLC Gates: Where the Build Either Holds or Doesn’t

Whether the institution is configuring a vendor platform, integrating modules, or developing significant custom code, the build phase must run through a secure software development lifecycle with mandatory security gates. These gates are not optional checkpoints; they are pass-fail criteria that block progression until satisfied. Programmes that allow gates to be deferred for scheduling reasons consistently regret it.

The minimum gate set for a core banking implementation includes:

Architecture review — security architecture sign-off of the proposed design before detailed build begins, with specific attention to trust boundaries, data flows, identity and authorisation model, encryption, segmentation, and integration patterns.

Code review — peer review of all custom code with explicit security review of authentication, authorisation, input validation, output encoding, cryptographic usage, error handling, and logging. For configuration-heavy implementations, the same discipline applies to configuration items, which are peer-reviewed and version-controlled.

Static application security testing (SAST) — automated scanning of source code for common vulnerability classes, integrated into the build pipeline so that critical findings block deployment.

Dynamic application security testing (DAST) — automated scanning of running applications for runtime vulnerabilities, run against each pre-production environment before promotion.

Dependency and software composition scanning — identification of vulnerabilities in open-source and third-party libraries, with a documented policy on permitted licences, critical-vulnerability remediation timelines, and a software bill of materials maintained for the lifetime of each release.

Secrets scanning — automated detection of credentials, API keys, and other sensitive material accidentally committed to source repositories, configuration files, or build artefacts.

Independent penetration testing — black-box and grey-box testing by an external party against the application, infrastructure, and integration surface, with a sign-off threshold that prevents go-live with unresolved high-severity findings.

Pre-go-live risk sign-off — a formal residual-risk acceptance by named accountable executives, with all outstanding findings catalogued, owned, and date-bound for closure.

These gates are not bureaucracy. They are the mechanism by which the security governance defined at programme start translates into the actual artefact that will go into operation. A programme that has documented all of the above and waived three or four gates in the final weeks before cutover has chosen to carry the unresolved risk into operations, where it will compound.

IV. Discipline Two: Enforce Zero-Trust Access and Strong Privileged-Access Controls

Core banking environments should never rely on the assumption that the internal network is trusted. NIST describes zero trust as a shift away from broad network perimeters toward the protection of users, assets, and resources individually, with each access decision verified explicitly, performed under least privilege, and made under the assumption that a breach has occurred or will occur. FFIEC guidance and equivalents stress access controls, logging, monitoring, encryption, and periodic access-right reviews as fundamental, not optional. These are the same conclusions reached through different vocabularies.

In practice, zero trust in core banking is less about adopting a particular product set and more about removing the architectural assumptions that have historically made lateral movement and privilege escalation easy once an attacker is inside the perimeter. The core sits within a controlled network zone; the database tier sits within a tighter one; the privileged administrative paths sit within a tighter one still; and every access decision is verified against identity, device posture, contextual signals, and risk score, not against network location alone.

| “You cannot ‘never trust, always verify’ while orphaned accounts remain active, privileged access is excessive, MFA coverage is incomplete, and joiner-mover-leaver processes are unreliable.” |

Multi-Factor Authentication, Done Properly

Microsoft's 2025 Digital Defense Report documented that, when properly deployed, MFA blocks over 99 percent of identity-based attacks, and that 97 percent of identity attacks rely on password-spray techniques against accounts whose credentials appear in known leaks. The operative phrase is "properly deployed." Partial MFA deployment, exemptions for legacy systems, push-fatigue susceptibility, session hijacking, and the absence of phishing-resistant MFA for privileged accounts are all conditions that enable credential abuse in institutions that believe they have solved the MFA problem.

For core banking, MFA should be required for all users with access to the platform, with no exceptions for legacy systems or service workflows. Privileged users, system administrators, database administrators, application administrators, batch operators, vendor support personnel, must use phishing-resistant MFA, meaning FIDO2 security keys, platform authenticators, or PKI-based authentication, not SMS or one-time-passcode applications that can be phished or relayed. Where legacy interfaces cannot support modern MFA, they should be brokered through controlled access points that enforce it, not exempted from it.

RBAC, ABAC, and Real Segregation of Duties

Role-based access control should be the default model for the core, complemented by attribute-based access control when role-based logic cannot be expressed cleanly. The discipline matters far more than the choice of acronym. Must Roles be defined functionally: What business activities does this person perform? rather than being copied from the previous system or designed around existing permissions. Each role should be the smallest set of permissions required to perform a defined business function, and each user should hold the smallest set of roles required.

Segregation of duties is the control that matters most for fraud prevention and the one most consistently weakened over time. The maker-checker pattern, where one user initiates and another approves, should be enforced at the application level for material actions, with explicit prevention of self-approval, single-user override, and after-hours bypass.

Beyond the maker-checker pattern, the segregation matrix should explicitly separate developer access from production administration, database administrator access from application administrator access, and operations access from security monitoring access. These boundaries should be defined in policy, encoded in the role model, monitored in production, and reviewed on a defined cadence.

| “Segregation of duties is the control most consistently weakened over time. The matrix must be defined in policy, encoded in roles, monitored in production, and reviewed quarterly.” |

Privileged Access Management for the Accounts That Matter Most

Privileged accounts such as system administrators, database administrators, application administrators, emergency accounts, service accounts, vendor support accounts, batch processing accounts, middleware accounts, and cloud platform accounts are the keys to the core. A privileged access management capability should vault credentials, broker access through controlled session managers, record sessions for high-risk activities, enforce just-in-time elevation rather than standing access, and rotate credentials automatically. None of these capabilities is exotic in 2026; mature products are available from multiple vendors, and the open-source ecosystem offers options as well. Whether the institution chooses to buy or build is less important than having a working capability in place before the core goes into operation.

Vendor support access deserves particular attention. The vendor's ability to access customer environments to provide support is essential to the operational model, but creates substantial risk. Vendor access should be on-demand, time-bounded, ticket-linked, recorded, and reviewable. Standing remote access for vendor staff, without per-session authorisation by the customer, is a control failure that should be treated as such, including in commercial negotiations, where vendors often resist the operational discipline required.

Just-in-Time Access, Session Recording, and Break-Glass

Just-in-time access, the principle that privileged rights are granted for a specific task, for a specific duration, and removed automatically afterward, eliminates the standing privilege that attackers and malicious insiders most reliably exploit. It is a substantial change to operational habit, and the operations team will resist it, but the resistance is the signal that the control matters. Session recording for high-risk activities provides the audit trail that makes both insider abuse and credential misuse detectable after the fact and deterrable in advance.

Break-glass procedures, the controlled emergency-access mechanisms used when normal access paths are unavailable, are the single most-abused administrative control in banking environments. They are necessary, but they must be tightly governed: pre-defined accounts with credentials held under split control, activation only with formal authorisation, automatic logging and notification, and mandatory post-use review. Routinely used break-glass access is not break-glass access. It is an unmonitored standing privilege under a different name.

Access Recertification on a Cadence That Means Something

Quarterly access recertification, performed by named owners with the authority and information to make actual decisions, is the control that prevents permission accumulation from becoming the dominant identity risk. The recertification must be substantive: each owner reviews each user's actual entitlements, signs off on each as still required, and revokes those that are no longer required. Rubber-stamped recertifications, performed under deadline pressure by managers who do not understand the entitlements they are confirming, produce paper compliance and zero risk reduction.

Secrets and Key Management

Secrets such as passwords, API keys, database credentials, encryption keys, certificate private keys, and OAuth tokens should never be hard-coded in source code, configuration files, scripts, or deployment manifests. They should be stored in a secrets management platform that handles versioning, rotation, access control, and audit logging. Encryption keys for production data should be managed in hardware security modules under split-knowledge and dual-control procedures, with the cloud provider's KMS as an acceptable equivalent where the institution's risk appetite and regulatory environment permit it.

The most common failure mode in this domain is not the absence of a secrets manager but the partial adoption of one: secrets in the vault for new services, but legacy services still using hard-coded credentials; rotation policies defined but not enforced; access to the vault itself not subject to the same disciplines as other privileged access. The mitigation is to treat the secrets management deployment as a programme in its own right, with completion criteria and ongoing assurance, not as a tooling project.

V. Discipline Three: Secure Data, Integrations, and Operational Resilience End-to-End

Core banking risk concentrates around customer data, transaction integrity, payment interfaces, third-party integrations, and service continuity. The third discipline is the one that protects these dimensions end-to-end, across the full path that data and transactions travel, rather than only at the perimeter of the core itself. NIST's supply-chain risk guidance and CSF 2.0's explicit inclusion of cybersecurity supply-chain risk management under the Govern function recognise what banking incidents have repeatedly demonstrated: an attack rarely begins or ends at the system you most carefully defended.

Encryption Everywhere It Matters

Encryption in transit and at rest should be applied to databases, backups, message queues, log streams, file transfers, APIs, reporting replicas, and every other location where customer or transactional data is stored or moved. The discipline is not new, and the technology is mature; what is consistently missed is the coverage audit. A bank that has implemented TLS for its external APIs but transmits data unencrypted between internal services, encrypts its production database but not its read replicas, and protects its primary backup. Still, the archive copy is not protecting its data. It protects a subset and exposes the rest.

Key management is the most commonly underbuilt aspect of banking cryptography. Institutions that get the cryptography right but mishandle the keys are no better protected than those that skip both. Keys should be generated, stored, rotated, and destroyed under formal procedure, with HSM-based protection for production keys, defined rotation cadences, and clear separation between key custodians and the operators of the systems that use the keys.

API Security: Where the Modern Core Actually Lives

Modern core banking platforms expose APIs to channels, fintech partners, payment service providers, regulatory and reporting integrations, and, increasingly, open-banking ecosystems. The API surface is now the dominant integration model and, accordingly, the dominant attack surface. The minimum control set for core banking APIs includes strong authentication (OAuth 2.0 with appropriate grant types, or equivalent), mutual TLS where the partner relationship justifies it, rate limiting calibrated to expected business volumes, schema validation that rejects malformed requests rather than processing them with unpredictable behaviour, replay protection through nonces or timestamps with bounded windows, and transaction-level audit trails that record both the API call and the business transaction it produced.

| “The API surface is now the dominant integration model in core banking. It is also the dominant attack surface, and most institutions monitor it as a network service rather than as a transaction channel.” |

An API gateway or equivalent control plane that brokers all external access provides a single point of policy enforcement and observability. Internal APIs should not be assumed to be safer than external ones; lateral movement after an initial compromise is exactly the path most adversaries take. Where internal integrations use message queues, file transfers, or batch interfaces, which are easy to overlook because they do not appear to be obvious attack surfaces, the same authentication, authorisation, and audit disciplines should apply.

Data Masking and Tokenisation in Non-Production

Non-production environments development, test, user acceptance, training, and performance accumulate copies of production data because realistic data is required for realistic testing. They are also subject to weaker access controls, looser monitoring, and broader access lists than production. Customer data in non-production environments, in clear text, is one of the most consistent root causes of large-volume data breaches in financial services.

The discipline is straightforward: production data should not be present in non-production environments. Masking, tokenisation, and synthetic data generation should be used to provide realistic but non-sensitive datasets. Where production data is genuinely required for a specific test scenario, its presence should be time-bounded, access-controlled, and removed immediately afterward. This requires tooling capability and operational discipline, both of which must be in place before the implementation begins generating environment copies, rather than being added later when several years of test data have already proliferated.

Immutable Logs, SIEM, and SOC Monitoring

Logs from the core platform, its databases, middleware, APIs, admin consoles, identity systems, and supporting infrastructure should be aggregated into a security information and event management platform that supports correlation, retention, and analytics across the full estate. The logs themselves should be written to storage that prevents modification after the fact, so that an attacker who reaches the core cannot retroactively cover their tracks by editing logs.

The SIEM and SOC monitoring must specifically cover, with tuned detection logic:

Privileged activity — every administrative action on the core, its database, its middleware, and its cloud platform, with detection logic that flags unusual timing, unusual volumes, unusual command sequences, and combinations of actions that should not occur together.

Failed and anomalous authentication — patterns of failure indicative of password spray, credential stuffing, or targeted compromise attempts, with both threshold-based and behavioural detection.

Suspicious account changes — creation of new accounts, modification of permissions, addition of users to privileged groups, changes to authentication methods, and modifications to service accounts.

Anomalous payment patterns — unusual transaction values, unusual destination accounts, unusual timing, deviations from normal customer behaviour, and patterns consistent with known fraud or money-mule typologies.

Failed transactions and reconciliation breaks — discrepancies between expected and actual postings, repeated reversals, batch failures, and patterns that may indicate manipulation rather than operational error.

Configuration drift — unauthorised changes to hardening baselines, network controls, monitoring rules, or security tooling, detected through comparison with known-good baselines.

Coverage matters as much as sophistication. The most common monitoring failure is not poor detection logic but the failure to monitor significant components at all. The database layer is logged, but events are not forwarded; middleware writes logs locally that no one reads; the cloud control plane has its own logging that no one integrates. A periodic audit of monitoring coverage against the asset and data flow inventory is essential.

Tested Backup, Restore, Disaster Recovery, and Cyber Recovery

Backups are the last line of defence against ransomware, destructive attacks, and catastrophic operational failure. They are also among the most overstated controls: institutions routinely claim backup capabilities they have never actually exercised and, during incidents, discover that the backups are incomplete, the restore process fails, the recovery time exceeds tolerance, or the backups themselves have been compromised.

The minimum backup discipline for a core banking platform includes immutable backups, protected against modification or deletion for a defined retention period, even by privileged users, stored in a separate storage environment, outside the blast radius of an attacker who has compromised the production environment. Encryption keys for backups should be managed separately from the systems that produced the backups. Backups should be tested by full restoration to an isolated environment on a defined cadence, and the restoration should be timed end-to-end to validate that recovery time objectives are achievable in practice, not only on paper.

| “A backup that has not been restored is not a backup. It is a hypothesis. Cyber-recovery exists to prove the hypothesis before the incident does.” |

Disaster recovery testing should exercise the full failover sequence, including human procedures, communication paths, dependent systems, and the return-to-primary process. Cyber-recovery, the specific scenario in which the primary environment is assumed compromised, and the recovery must be performed under the assumption that the attacker may still be present, should be planned and tested as a separate discipline from operational disaster recovery. The procedures, decision rights, and timelines differ. So do the technical requirements: cyber-recovery often demands a clean-room rebuild rather than a failover, and the recovery point objective is measured backward from the point of compromise, not from the point of failure.

Each of these capabilities must be tested before going live. Untested backup and recovery capabilities are not capabilities; they are intentions. The number of institutions that discover this distinction only during a serious incident remains depressingly high in 2026.

VI. Special Focus: Securing Mifos X and Apache Fineract Open-Source Core Banking

Apache Fineract and the broader Mifos initiative that builds on it have become among the most widely deployed core banking platforms in the world, particularly among microfinance institutions, digital banks, cooperative banks, and emerging-market financial inclusion programmes. It powers institutions serving hundreds of millions of customers across Africa, Asia, and Latin America. It is also open-source, Apache-licensed, and freely available. These properties make it a strategic choice for many institutions; they also create a security profile that differs from that of closed vendor platforms in ways institutions must understand and manage explicitly.

What Open-Source Core Banking Changes

The same three disciplines, governance from day one, zero-trust access, and end-to-end data and integration protection, apply to Fineract deployments without modification. What changes is the distribution of responsibility and the specific implementation patterns through which the disciplines must be enforced. Three properties of open-source core banking deserve particular attention.

First, the source code is public. This is generally a security advantage in the long run: the code receives review from a global community, and Apache's software foundation governance imposes a measure of discipline on releases. But it also means that vulnerabilities are visible to attackers as soon as they are to defenders. The institution must actively track upstream releases, security advisories, and CVE disclosures and have the operational capability to apply security patches promptly. The institution that runs an unpatched Fineract release for 18 months because no one is responsible for upstream tracking has accepted a risk that a commercial vendor would at least have flagged in a support communication.

Second, operational responsibility lies entirely with the institution or its chosen implementation partner. There is no vendor with a contractual obligation to deliver security patches, monitor production environments, or respond to incidents. The institution must build or contract for every aspect of the operational capability: deployment, hardening, patching, monitoring, backup, and incident response. Where the institution lacks the internal capability, which is common in the smaller institutions for whom Fineract's cost profile is most attractive, the implementation partner must be selected with the same diligence applied to a vendor relationship. The contractual structure must be explicit about security responsibilities.

Third, the deployment patterns vary widely. Fineract is most commonly deployed as a Java application stack, historically Tomcat-hosted, increasingly Spring Boot-based, backed by MySQL, MariaDB, or PostgreSQL, often running in Docker containers on Kubernetes, often hosted on AWS, Azure, GCP, or local cloud providers. The Mifos X stack adds the Community App user interface (typically AngularJS or modern Angular), mobile applications, and integration components. Each of these layers has its own security requirements that must be addressed; the security model is not the platform's alone but the composition of every component the institution deploys.

| “Open-source core banking does not reduce security responsibility. It moves it. Every control that a vendor would have provided becomes the institution’s responsibility to design, implement, and maintain.” |

The Three Disciplines, Applied to Fineract

The first discipline, security governance from day one, applies with particular force to Fineract deployments, because the absence of a vendor means there is no second line of defence outside the institution. The control mapping should explicitly include the Apache Fineract codebase, its dependencies, the surrounding Mifos X components, the deployment platform, and the integration layer. Threat modelling should consider the public visibility of the source code, known attack patterns against Java web applications, the specific exposure of the REST API, and the database access paths. The secure SDLC gates should apply to every customisation, every configuration change, and every deployment manifest, with particular attention to dependency management.

Specific governance considerations for Fineract include:

Upstream tracking — formal monitoring of the Apache Fineract project, the Mifos community releases, the Apache Software Foundation security mailing lists, and the CVE databases for the underlying Java, Spring, Tomcat, Hibernate, Jackson, and Log4j stacks. Log4Shell in late 2021 demonstrated how a vulnerability in a transitive dependency can affect every Java-based core banking deployment globally; institutions that did not have upstream tracking in place at the time discovered they were exposed by reading the news.

Software bill of materials — a maintained SBOM listing every dependency, version, and licence, automatically refreshed against vulnerability databases, with a defined remediation policy for high and critical findings.

Patch cadence policy — a documented standard for how quickly security patches must be applied (typical mature practice: 14 days for critical, 30 days for high, 90 days for medium, for internet-facing components), with exceptions formally accepted, owned, and date-bound.

Build pipeline integrity — controls on the Maven or Gradle build process, including dependency pinning, signature verification on artefacts, and SAST/DAST scanning of every build before promotion.

The second discipline, zero-trust access and privileged access control, applies to Fineract through both the application's built-in capabilities and the surrounding infrastructure. Fineract ships with role-based access control, a maker-checker workflow capability, audit logging, and (in current releases) support for two-factor authentication. These capabilities should be enabled, configured, and tested. The frequent failure mode is to deploy Fineract with the default administrative credentials still active, two-factor authentication disabled, maker-checker rules unconfigured for sensitive operations, and the Tomcat or Spring Boot admin endpoints exposed to networks they should not be exposed to.

Specific zero-trust considerations for Fineract include:

Default credentials — every default administrative credential (‘mifos’, ‘admin’, ‘app_admin’, database ‘root’, and equivalents) must be changed before the platform is exposed to any network beyond the build environment. This is the most exploited issue across open-source platforms, and Fineract deployments are no exception.

Two-factor authentication — enabled for all users, phishing-resistant for administrators. Where Fineract’s native 2FA does not meet the institution’s requirements, an identity provider integration (OIDC, SAML) should be configured to broker authentication through an enterprise identity platform that does.

Maker-checker enforcement — configured for every sensitive operation in the platform, including account opening, large-value transactions, customer data modifications, fee waivers, loan write-offs, and administrative actions. The default configuration is permissive; the production configuration should not be.

Role definition — application roles defined functionally and reviewed by business owners, not copied wholesale from a reference deployment or assigned with maximum permissions “until we figure out what each role needs.”

Privileged access to the platform — database administrator access to the Fineract schema, operating-system access to the application servers, container-orchestration access to the Kubernetes cluster, and cloud-platform access to the underlying infrastructure, all governed through a privileged access management capability with vaulting, session recording, and just-in-time elevation.

REST API exposure — the Fineract API surface should never be exposed directly to the public internet. An API gateway should sit in front of it, enforcing authentication, rate limiting, schema validation, and audit logging. Internal services that consume the API should authenticate using the same disciplines applied to external consumers.

Administrative endpoints — Spring Boot Actuator endpoints, Tomcat manager interfaces, container orchestration dashboards, and database administration consoles must not be reachable from production networks except through bastion hosts under privileged access controls.

The third discipline, end-to-end data integration and resilience protection, applies to Fineract with specific implementation patterns. The PostgreSQL or MySQL database should be configured for transparent data encryption, with keys held outside the database server. TLS should be enforced for every connection: between the user and the web tier, between the web tier and the API, between the API and the database, and between the platform and every integration. Backups of the Fineract database should be encrypted, stored in immutable storage outside the production environment, and regularly tested through full restoration.

Specific data and integration considerations for Fineract include:

Database encryption — at-rest encryption configured at the storage layer (cloud-native or database-native), with key management performed through a KMS, HSM, or equivalent capability under the institution’s control. Application-layer encryption of particularly sensitive fields (KYC documents, payment instructions) provides defence-in-depth.

TLS configuration — modern cipher suites only, deprecated protocols and ciphers disabled, certificates managed through an enterprise certificate authority, regular scanning to detect drift.

Tenant isolation — Fineract’s multi-tenant capability is widely used, particularly in shared infrastructure deployments for groups of microfinance institutions. The tenant separation model must be understood, configured correctly, and tested under adversarial conditions to ensure that data does not cross tenant boundaries either through the application logic or through database-level access paths.

Non-production data — customer data not present in development, test, training, or demo environments. Synthetic datasets generated for testing purposes, or production data anonymised through validated processes.

Logging and SIEM integration — Fineract audit logs, application logs, database logs, container logs, and cloud platform logs forwarded to a SIEM with detection logic tuned to the platform’s specific event patterns. Default Fineract logging is functional but not security-monitoring-grade out of the box; the institution must invest in tuning.

Backup and cyber-recovery — automated backups of the database and configuration, held in immutable storage with encryption keys separately managed, tested by full restore on a defined cadence. The restore should specifically include the test of bringing a fully functional Fineract instance back from backup, not only the test of file integrity.

Integration security — payment switch integrations, channel integrations, agency banking integrations, mobile-money provider integrations (M-Pesa, MTN MoMo, Airtel Money, equivalents), and regulatory reporting integrations all subject to authentication, authorisation, audit, and replay protection. Mobile-money integrations in particular are a high-fraud-risk surface in microfinance deployments and demand specific attention.

None of the above requires capabilities that are unavailable in the open-source ecosystem. Excellent open-source tools exist for identity management (Keycloak), API gateway functionality (Kong, APISIX), secrets management (HashiCorp Vault), SIEM (Wazuh, OpenSearch-based stacks), backup (Velero for Kubernetes, restic and equivalents), and most other categories. The work is in selecting, integrating, hardening, and operating them as a coherent platform, and in not deferring that work until after go-live.

Apache Fineract is a credible core banking platform. The credibility depends entirely on what the institution builds around it. The security maturity of the deployment is the security maturity of the institution, with nothing left over.

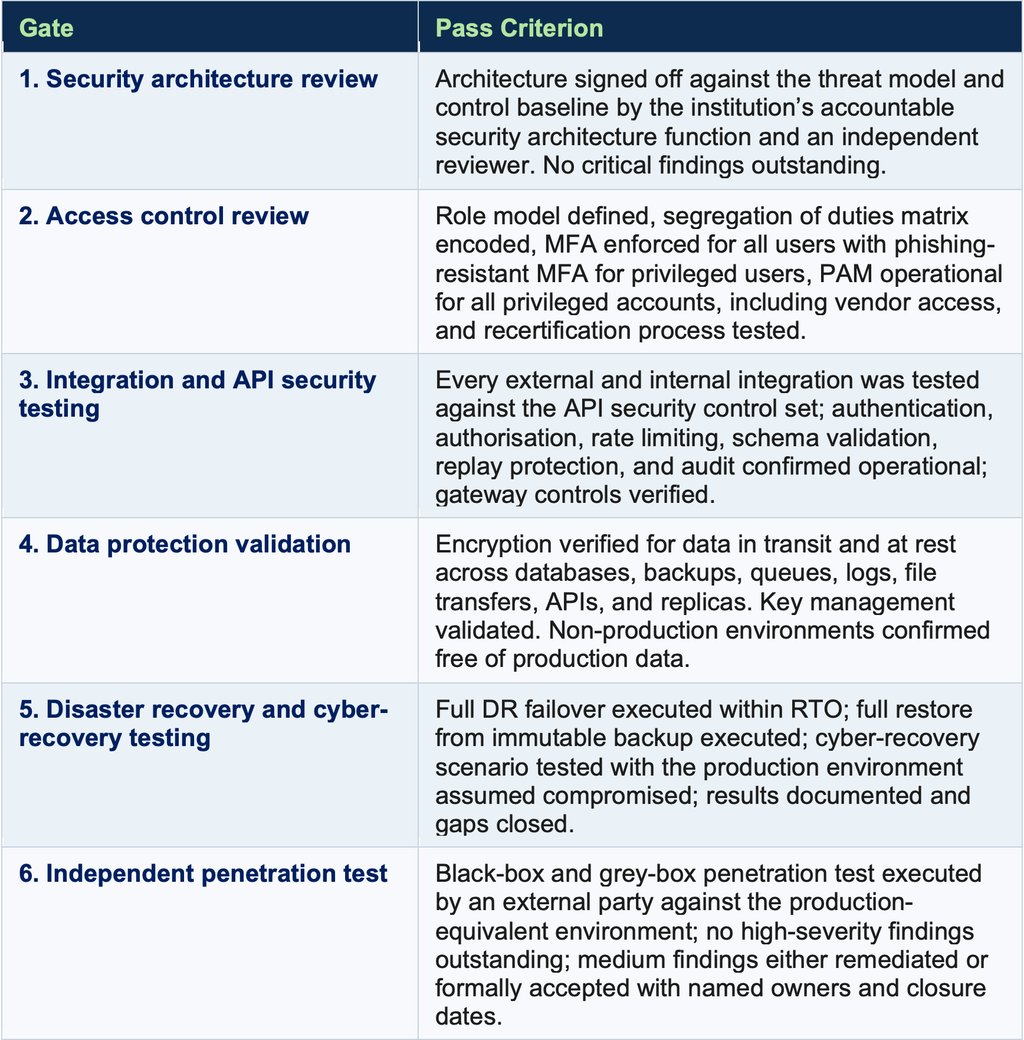

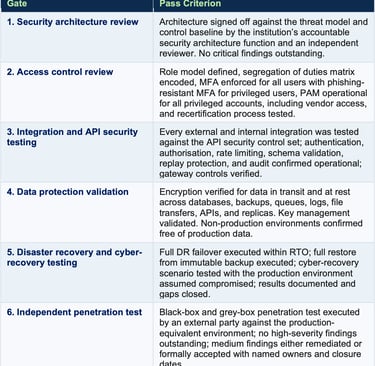

VII. The No-Go-Live Rule: Six Gates That Must Be Passed

The single implementation rule that prevents the largest category of post-go-live incidents is the simplest: no core banking go-live should proceed without passing six security gates. Each gate is a pass-fail criterion, owned by named individuals, with evidence retained for examination by internal audit and regulators. Gates may not be waived to meet a schedule. A programme that cannot pass these gates should not go live, and the decision to defer go-live until the gates are passed is invariably less costly than going live with them unresolved.

These six gates do not replace the regulatory readiness assessments that supervisors require. They precede them. An institution that passes its six gates is also well positioned to satisfy the regulator's go-live attestation; an institution that has not passed them rarely satisfies the regulator either, and the regulatory finding adds delay, cost, and reputational drag to a programme already under pressure.

VIII. Conclusion: Protecting the Ledger Forever

Core banking is the system on which the institution stakes its ability to function. The decisions made before its implementation, during its build, at its cutover, and across the operational decades that follow determine whether the institution carries an exposure it will eventually pay for or a platform it can defend with confidence.

Three disciplines decide the outcome.

Security governance built into the programme from day one ensures that the system's controls reflect the threats the institution actually faces, the regulatory frameworks it operates under, and the risk appetite it has explicitly accepted.

Zero-trust access with strong privileged-access controls ensures that the most-exploited modern attack paths, identity compromise, credential abuse, and lateral movement through over-permissioned accounts do not find the easy access they routinely do find.

End-to-end protection of data, integrations, and operational resilience ensures that, when an incident occurs, the damage is contained, the recovery is genuine, and the institution emerges intact.

These disciplines apply whether the platform is a vendor suite, a legacy mainframe, a modern cloud-native stack, or an open-source deployment of Apache Fineract. The implementation patterns differ. The disciplines do not.

| “Protect where the attacker is, not where they were. And build the governance structures that force the security programme to keep asking, every quarter, every budget cycle, and every board meeting, whether those two things are still the same.” |

The chained benchmark problem identified in the preceding article in this series, the tendency of security programmes to remain anchored to the threat landscape of previous years, affects core banking with particular force, because the platforms themselves change so slowly.

The disciplines described here are the mechanisms by which a slow-changing platform is kept aligned with a fast-changing threat environment. They are not a one-time achievement. They are a continuous discipline whose evidence the board should expect to see, the regulator should expect to examine, and the operational teams should expect to demonstrate, every quarter, for as long as the platform runs.

KEY RECOMMENDATIONS SUMMARY

Governance Actions

Establish security as a core workstream in every core banking programme, with named ownership, defined budget, regulatory mapping, threat model, and risk appetite in place before design begins.

Map controls to NIST CSF 2.0, ISO 27001, PCI DSS, the SWIFT CSP, and all applicable central-bank expectations as a single living artefact, maintained for the life of the platform.

Define the six mandatory go-live gates and enforce them without waiver — security architecture review, access control review, integration and API security testing, data protection validation, DR and cyber-recovery testing, and independent penetration test.

Programme Actions

Enforce phishing-resistant MFA for all administrators and high-risk roles, and conventional MFA for all users, with no legacy-system exemptions left unbrokered.

Deploy privileged access management before the platform enters production, covering system, database, cloud, batch, middleware, and vendor support accounts, with just-in-time elevation, session recording, and quarterly recertification.

Implement HSM-based or KMS-based key management for all production cryptographic keys, with no hard-coded credentials and no static secrets in source repositories.

Build an immutable backup and cyber-recovery capability before go-live, tested by full restoration on a defined cadence, with cyber-recovery procedures separate from operational disaster recovery.

Apache Fineract / Mifos-Specific Actions

Track upstream Apache Fineract releases, dependency CVEs, and ASF security advisories through a documented capability, with patch cadence policy enforced (14 days critical / 30 days high / 90 days medium for internet-facing components).

Change all default credentials, enable two-factor authentication, configure maker-checker for all sensitive operations, and broker the REST API through a hardened API gateway — every one of these is a frequent source of compromise in Fineract deployments.

Treat the implementation partner as a vendor relationship for security purposes, with explicit contractual responsibilities for hardening, patching, monitoring, and incident response where the institution does not perform these in-house.